Mortgage & Wealth Strategies

Say Hello To The Easiest Way To Mortgage

.png)

Beyond The Rate

As expert mortgage brokers, we know building wealth through homeownership and achieving financial freedom is about more than just chasing the lowest rate—it’s about strategy.

We're taking you behind the scenes and giving you the insider tools and powerful strategies to get ahead. If you’re a first-time homebuyer, you’ll find everything you need to secure your first property and start building wealth from day one.

If you’re an existing homeowner, this is where you take control. Maximize the wealth-building potential of your current home with proven strategies for refinancing, leveraging equity, and optimizing your mortgage for bigger opportunities.

Your mortgage is more than a loan—it’s a gateway to long-term financial success.

Our goal is simple: to equip you with the knowledge and tools to make smart, strategic decisions that will transform your financial future.

Let’s get started.

Inflation’s Not Cooling Yet —But Should You Sweat It?

July 22, 2025 | Posted by: Matt Broom-Hall

.png)

It’s late July, and while summer weather may be mellow, the mortgage market is heating up—just not in the way buyers or homeowners were hoping.

New inflation data has once again put the brakes on rate-cut optimism, and lenders have already begun nudging up fixed mortgage rates. If you were hoping for more relief by fall, it's time to take a closer look at the numbers and what they really mean. Let’s dig in.

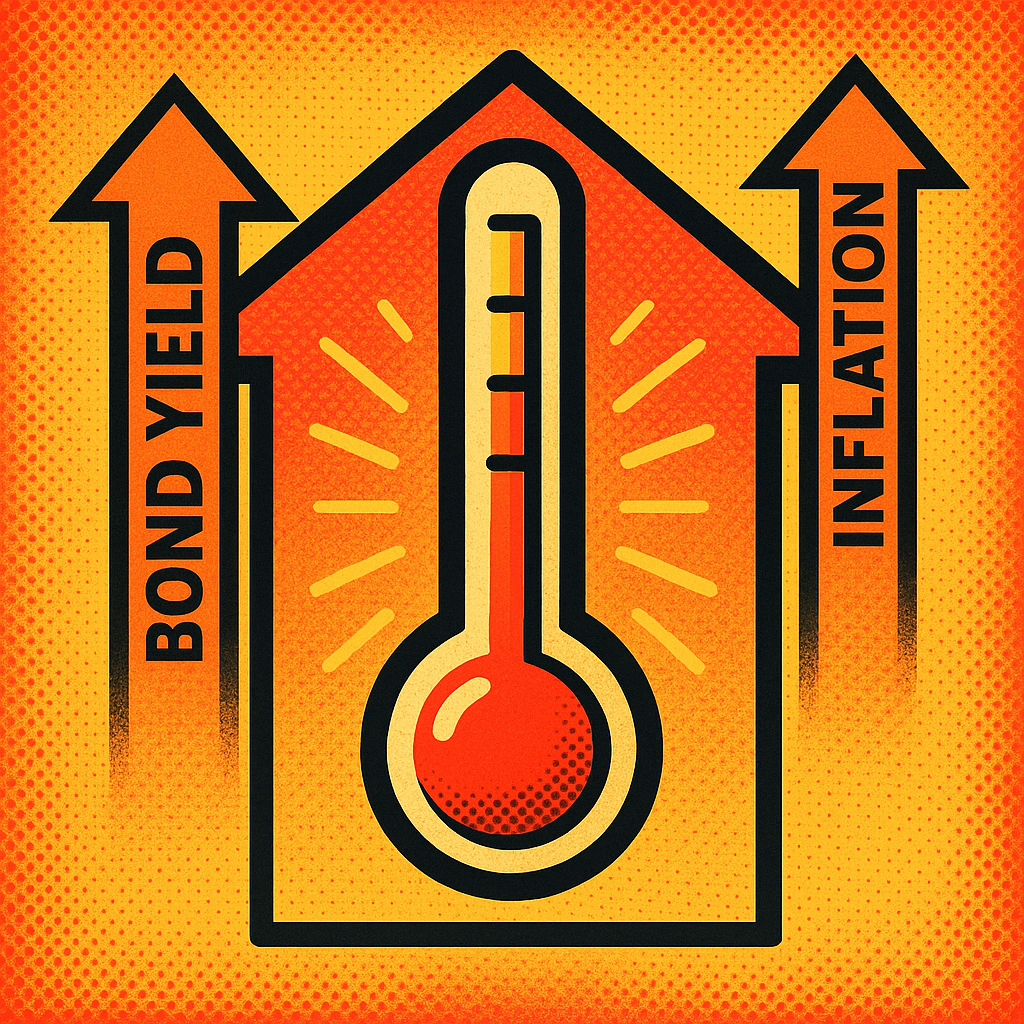

Last week’s inflation readings for June didn’t deliver the cooling we needed—not in Canada, and not in the U.S. While overall inflation ticked up slightly to 1.9% year-over-year, core inflation (what the Bank of Canada really watches) stayed stubbornly at 3%. In other words, we’re still not where the Bank of Canada feels comfortable pulling the trigger on another rate cut.

Bond markets reacted swiftly. Canadian bond yields made another jump, especially after U.S. data showed similar upward trends—driven, in part, by new tariff-related price pressures. That’s key because fixed mortgage rates move with bond yields—and sure enough, lenders have bumped up fixed rates across the board.

For variable, the market’s no longer expecting multiple cuts this year. Right now, the forecast is just one small 0.25% cut in 2025—if the economy allows. But I still think the Bank of Canada will need to go further. Shelter costs—one of the main drivers of inflation—are finally starting to cool, and our overall economic momentum is slowing. If that continues, we may need a more supportive rate closer to 2% to keep things moving.

Insider Strategy

Canadians still have more mortgage flexibility than many think. Most mortgages come with built-in prepayment privileges—usually up to 15% or 20% annually. That means you could slash years off your loan and save thousands in interest, simply by topping up your payments when you can. Definitely worth reviewing!

You can learn more about prepayments in this post from my strategy vault: Don't Forget About Your Prepayment Privileges: They Can Unlock Savings & Save You Thousands

Mortgage Selection Advice: Fixed or Variable?

Right now, five-year fixed rates are priced about the same as three-year terms. That gives borrowers the option of locking in longer-term stability without paying a premium.

If you’re starting fresh and value predictability, a fixed rate might be your best call—it shields you from future increases and brings peace of mind in an unpredictable market.

But if you're already in a variable rate, now is not the time to lock into a fixed. Fixed rates have recently climbed, and switching now could mean locking in at the top—not ideal if rates are expected to fall over the next 12 to 24 months.

Variable rates could still come out ahead in the long run—if inflation cools and the Bank of Canada continues to cut. That path won’t be without bumps, so it only makes sense if you’re financially comfortable riding it out.

Bottom line: Fixed is the safe bet for new borrowers. Variable might still win for those already in it—just don’t make a move out of fear.